GameStop Valuation Analysis – A Framework to Value a Moving Target

As promised, this GameStop valuation analysis will offer a quick and simple framework to assign a fair market value today to GameStop. I will not get too scientific in this exercise, as keeping it simple, while always a good idea, is especially so at this stage of the company’s turnaround.

If you haven’t already, I would recommend first reading my overall GameStop investment thesis, as the multiples and premiums in this analysis are of course rooted in the conclusions of the original note.

TL/DR: Using a hybrid of adjusted book value multiplier and sum of the parts methodologies, I arrive at a current fair price of the company today of $33B, or ~$74/share.

Before I go any further, let’s bring back the meme from the first note to get this out of the way for any new readers:

As discussed in the first note, while there is certainly some value that should be assigned to right tail event outcomes, these are only a cherry on top of an already sound investment foundation. The fear of looking like Big Bird in the board meeting appears to truly have put a ceiling thus far on the stock.

Investment Thesis Summary

First, a quick refresher on the overall investment thesis before getting to valuation analysis:

· Ryan Cohen & Board Incentive Alignment – 100% aligned to long-term shareholders; they are fellow shareholders who receive zero compensation.

· Balance Sheet Strength & Profitability – Nearly $9B of cash and equivalents, 4,710 Bitcoin, and right-sized with growing profits.

· Organic Growth Initiatives – Collectibles, PowerPacks, and Push Start Arcade all offer real reason for excitement.

· “Monetize the Apes” M&A Possibilities – My personal view that a retail conglomerate M&A strategy offers compelling accretive value given the ability to activate a shareholder base that is ready to support the company.

· The Tesla Effect (Reflexivity) – Any past mispricing is ancient history, the company has stored value on its balance sheet and is now valuable.

· Reddit Theories and Pumps as a Bonus “Call Option” – Only an added kicker, not the investment thesis.

· Volatility Breeds Income Opportunities – Drawdowns provide buying opportunities, upside events provide opportunities to harvest gains/lower cost basis.

Valuing A Moving Target

So all of this bullish rationale makes sense, but how the heck do we value this thing to know whether the company is undervalued?

Discounted cash flow analysis is an imprecise exercise today with the company undergoing tectonic shifts in the business, resulting in uncertain but promising future cash flows. We just don’t have enough information to use DCF.

Applying earnings or sales multiples is also useless given the shifting currents in the business as the company right-sizes legacy operations, kicks off its organic growth initiatives, and for now mostly preserves future earnings optionality on its balance sheet until investments are made. This means that both sales and earnings are inherently understated compared to company value, and that these ratios will of course be high compared to other retailers given the small denominator.

But we have to value the stock somehow, and I find it best to do so via an adjusted book value basis and sum of the parts hybrid methodology, since this allows us to reflect the company’s fortress balance sheet, assign a premium to reflect the brand/community value that is not present on the balance sheet, and to assign value to the upside event possibilities that is inherent in the stock.

Adjusted Book Value Component

Book value is the only stable denominator available today for GameStop, because earnings and revenue are temporarily and intentionally suppressed while the company restructures.

The price to book value ratio for GameStop at the time of this writing is a bit south of 2, which on the surface doesn’t look so bad if the company is just a struggling retailer turning around the business. But as we have covered, GameStop is much more than that.

First of all, GameStop’s book value is unusually clean for a retailer and deserving of a premium multiple on that basis alone, as it is comprised primarily of cash and Bitcoin. Typically, with a retailer we are looking at roughly half of assets being inventory, with the rest being a mixture of right-of-use assets from leases, intangibles/goodwill, other capitalized assets (machines, buildout costs, fixtures), and a small amount of cash (receivables are usually de minimis). Most of these assets are typically optimistically stated, whereas with GameStop the asset values are rock solid.

Since GameStop’s financials assign $0 for intangible assets, let’s add a very conservative $1B to the company’s book value to account for the company’s intellectual property and goodwill for its existing business and organic growth efforts.

Given Best Buy’s goodwill & intangibles value of $1.4B, assigning $1B to GameStop feels more than reasonable.

Let’s then also assume another conservative $1B in intangible value for the fact that any organic growth or M&A activities will automatically receive a “GameStop halo effect”, as the company’s loyal community rushes to support any new company initiative or acquisition. GAAP does not capitalize brand, community, or reflexive network value, which materially understates GameStop’s economic value relative to peers given its critical advantage there. I don’t compare this to Best Buy because Best Buy’s intangible assets don’t include this either, this should be viewed as GameStop’s community premium over comparable retailers.

The additional $2B brings us to a total adjusted book value of roughly $7B.

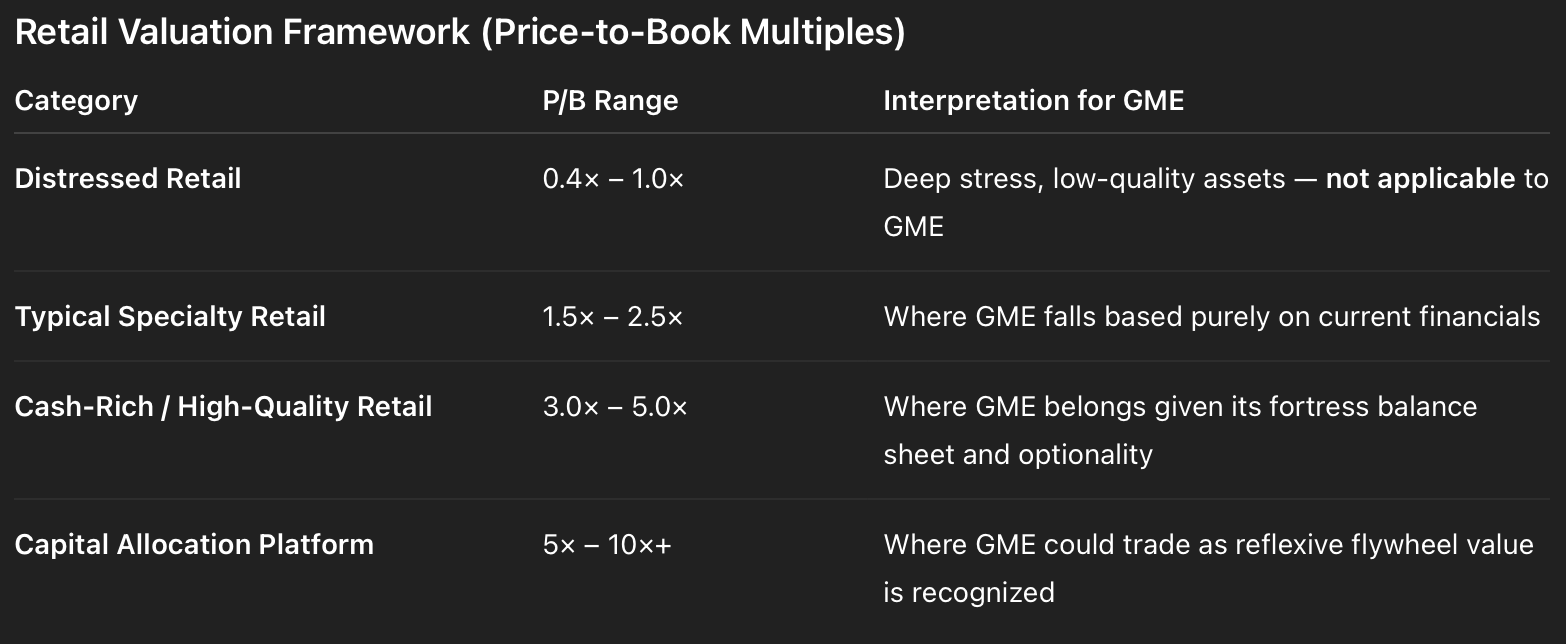

Now that we have an adjusted book value, moving on to P/B multiples since we are keeping it simple I find ChatGPT’s summary of retailer price to book value summary sufficient:

The point here isn’t precision; it’s to anchor GME within the broader retail valuation landscape and then adjust for its unusually clean balance sheet and optionality.

Even the above chart I find conservative when I see names like Best Buy sporting a P/B of 6x, with almost half their assets being comprised of lease assets or goodwill/intangibles having essentially no liquidation value!

But let’s keep it simple and very conservative, because we made the book value adjustments and I like to sleep at night. Assigning only a 4x P/B value against our adjusted book value of $7B, that gets us to a $28B company valuation.

Upside Event Possibility Value

While it is very much not the primary basis for my bull case, like it or not the fact is that GameStop does have strong event-driven tailwinds that could produce right tail events in the stock price. Whether it’s “meme names” melting up due to inflationary fiscal or monetary policy, another Roaring Kitty cycle, or if any of the Reddit community conspiracy squeeze theories turn out to have merit, the stock price enjoys violent rapid appreciation potential.

This is no scientific valuation method as there is no economic way to value this element other than to use other “meme values” as a proxy to reflect that the market does assign value to memes that are fundamentally worthless. Using meme coins as a proxy given their otherwise uselessness, I put GameStop’s “meme value” somewhere between Dogecoin’s ~$23B and Fartcoin’s $300M, but haircutting it down to a still substantial $5B given that it’s the original “meme company” likely to demand a continued premium and cult following. This feels conservative to me given that the comparable assets have far less substance than GameStop with no way to translate market cap into economic value.

Total Company Value

Worth noting in both components, once the above value is properly reflected in the stock price, GameStop can then crystallize this appreciation through share or convertible note issuance, further fortifying its balance sheet and exercising its reflexive flywheel advantage over competitors.

Adding the $5B of meme value to the $28B company value that we previously calculated based on adjusted book value, we get to a total company value of $33B.

On a per-share basis, this gets us to about $74/share, well above today’s price of under $21. Very undervalued, even through what I feel is an overly conservative lens.

Parting Thoughts

It’s an imperfect science, especially with a name like GameStop in the midst of a reflexive turnaround, but I feel the above exercise puts some logic behind the claim that the company is significantly undervalued and provides a conservative estimate for what a fair value might be for the company.

In summary:

· Adjusted book value = $7B

· Conservative BV multiple = 4x

· Fair value = $28B + $5B “meme” value = $33B, or ~$74/share

As the company executes on its strategy, its value will become increasingly difficult to ignore and as such I expect a reasonable fair value estimate to continue to grow alongside that success.

If there is any reader pushback to any of the above analysis or conclusion, please reach out or comment below, as I would love to hear it!

But as far as I can tell, the market and media has a hard pill to swallow about GameStop:

All content from Easter Egg Capital is for informational and entertainment purposes only. Nothing here should be taken as financial, investment, or trading advice – especially so for this post!